Buy The Dip: Private equity, the prime broker nexus and America's non-landing

The deep cuts of my 5k word PE opus magnum

It’s finally getting lighter and warmer here in Oslo, and it’s remarkable how much that helps lift spirits after a grim Nordic winter. I’m even getting the kids out the door in the morning without threatening hellfire and lifetime Nintendo bans.

It also gave me the energy to finish a chunky article I’ve wanted to write since November, on whether the Norwegian sovereign wealth fund should start investing in private equity.

I don’t actually cover Norway, or Norges Bank Investment Management – that’s my fantastic colleague Richard Milne – but I thought it was a good excuse to do a thorough examination of the broader investment case for (and against) against private equity. The result clocked in at over 5,000 words and featured one SpongeBob meme.

That’s probably more than what most people want to read about any one subject, but the reception was gratifyingly positive. So I thought I’d use this week’s newsletter to expand on a two issues that I didn’t have space to include even in a 5k word salad.

1️⃣ I chose to completely ignore any societal aspects of private equity.

There are a lot of people that viscerally hate private equity, what it represents and what it supposedly perpetrates. Just in the last year there have been two scathing books published on the industry, with the unsubtle titles Plunder: Private Equity’s Plan to Pillage America, and These Are The Plunderers: How Private Equity Runs – and Wrecks – America.

I haven’t read either, but I thought a metastudy published by the British Medical Journal on private equity’s impact on healthcare was damning enough for us to cover on Alphaville. I’ve seen one too many dividend-recap and NAV loan to not be a little cynical about the industry’s own narrative of heroic value creation. It’s telling that PE gets a bad rap even in inside finance.

I’m a bit wary of overly moralistic, often simplistic assertions, and try to be aware of my own (potential and actual) biases. Too many people lazily think that private equity (or banks, hedge funds etc etc) is somehow inherently wrong, or even evil. But for every debacle you can probably find a success story. I can genuinely see a case for private equity’s value to society.

But think it comes with enough caveats - for example, more “efficient” balance sheets that are fragile whenever there’s an economic downturn - that I decided that a nuanced, thorough exploration of this angle was a giant rabbit hole too far. Maybe some other time.

That said, I think its a bit unsavoury that the industry is arguably largely built on and sustained by government subsidy: the tax-deductibility of interest payments in many major countries. The carried interest issue is well-known, but if I was omnipotent for a day, a gradual but irrevocable unwind of debt subsidies would be one of my first acts.

2️⃣ I didn’t spend much time on NBIM’s unique aspects and the idiosyncratic reasons why private equity is a poor fit.

Obviously there was a fair amount of discussion of NBIM’s investment case, given that its desire to add PE to its mandate was the main reason for writing my post. But I didn’t want to go overboard on it either. This was primarily a post on private equity, not on NBIM.

So here are a few additional reasons for and against specifically NBIM getting into private equity, which I could’t fit into the original post.

The pros:

👍I think the transparency arguments against PE’s inclusion are overdone. Yes, the kind of detailed information that NBIM gives to the public is hard to reconcile with an inherently opaque industry. But the reality is that most Norwegians don’t really care about the transparency. It’s performative. This is helpful given the political optics, but of limited practical value. So I don’t see any insurmountable challenges here.

👍 I also called NBIM “the ultimate large, liquid, long-term investor [which] can harvest an illiquidity premium til the cows come home”, but this bears repeating and expanding. Unlike almost any other large pool of capital, NBIM has near-zero need for liquidity: the government generally only taps it for about 3 per cent a year (the long-term expected real return). Barring Ragnarokk, it can safely lock up enormous sums of money in private markets – if it makes financial sense to do so.

👍 Another issue that I mention but could have done with even more discussion is the argument that as a paragon of Bill Sharpe’s “market portfolio”, NBIM should get into private equity (and do far more in real estate and infrastructure). If you think that diversification is the one free lunch in finance, then eschewing private markets doesn’t make logical sense. And certainly not when public markets are atrophying a little.

The cons

👎 NBIM CEO Nicolai Tangen’s argument that this is a good time to get into PE because rising rates have caused lucrative capital shortages is very weak. And Tangen – a very smart guy – knows it.

Not just because of the darkening long-term outlook for returns - which my Alphaville post explored - but because it ignores the fact that ramping up in private equity is going to take a long time. What stage we happen to be in the financial cycle just shouldn’t even enter into the discussion. Making the timing argument would have been weird even in the depths of the 2022 bear market, but saying there’s a shortage of capital today – with many stock markets trading at or near record highs, credit markets healthy and private equity sitting on $2.59 TRILLION of “dry powder”– is plain wrong.

Tangen has compared getting into private equity to NBIM ratcheting up its equity weighting after the financial crisis, which turned out to be phenomenal timing. But with private equity we aren’t talking about public securities that NBIM can easily scoop up at a discount in volume. If NBIM is going to do this, it will have to be a strategic, multi-year effort (in reality probably multi-decade).

👎 However, most of all I think that NBIM itself - and any private equity firms hoping to have it as a big investor - radically underestimate the rod it will create for its own back because of the earlier point made in this newsletter.

Rightly or wrongly, PE is a controversial industry. And every time any private equity firm with NBIM money runs into any kind of controversy – and lord knows there always will be something – the Norwegian press will rake it over the coals. When it’s a broad, diversified investor in thousands of companies it can shrug helplessly and say the odd snafu comes with the territory. That won’t work as well with private equity investments.

Honestly, I laugh just thinking of the collective hissy fit that the country will go through when KKR/Blackstone/Carlyle/TPG etc blow up some hospital group, toy company or social housing project with “OUR MONEY!!”. For that reason, NBIM is likely to end up being fickle money that will do badly out of any PE adventure, even before the more nuanced financial arguments I tried to lay out in my Alphaville post.

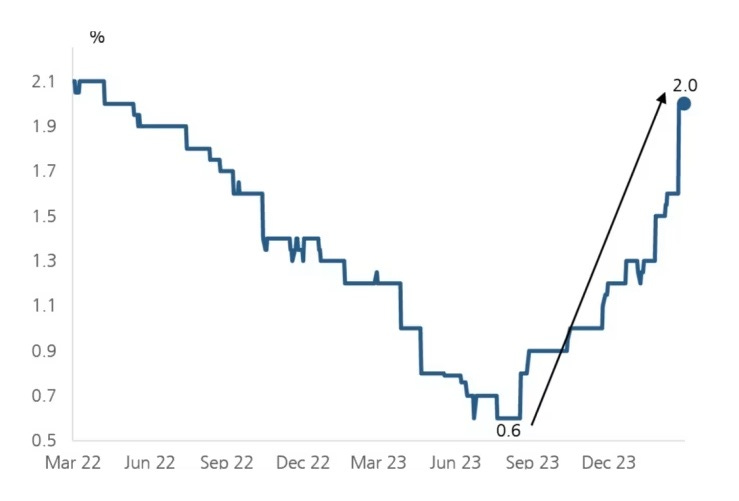

Anyway, on a completely unrelated and more positive note, here is my chart of the week, showing the remarkable bounce in consensus forecasts for US economic growth in 2024:

And here are this week’s links:

📈 Meet the American brokerage exec who’s rolling out the first publicly traded multi-club model. Here’s your chance to invest in Mongolia’s ninth best team.

📈Flash GDP numbers are systematically pessimistic. Why?

📈 Skechers’ family troubles. Nepotism: harder than you think

📈Are structured products to blame for suppressed volatility? The BIS thinks so.

📈 Apparently 97% of Americans have head of the Basel Endgame. Gotta love US lobbyist/fantasists.

📈Avid Bioservices had an oopsie. Killer opening line: “Bond markets have always been a pedantic person’s playground.”

📈 Italy, Europe’s unlikely outperformer. This one weird trick will supercharge your economy.

📈 It’s SPIVA time. Once more unto the ‘active comeback’ breach.

📈 The hedge fund-bank nexus. The BIS is oogling prime brokers.

📈 An empty Budget for the City. Craig Coben was unimpressed with the BRISA (as was AJ Bell and Citi)

📈 Some chemicals last forever. Some grace periods do not. Alex takes a look at the Chemours debacle.

📈 Buy the dip! Or, don’t. Not a slight on this newsletter. Actually a very thorough look at the historical success of dip-buying in various markets.

📈 The increasingly silly search for Europe’s (less) Magnificent Seven. Inspired by this fun post I also revisited the success of other Bloody Ridiculous Investment Concepts, like CIVETS and MINT.

📈 US companies are still very profitable. Digging into Goldman’s margins report.

📈 People are worried (again) about bond market liquidity. But what they should be thinking about are the consequences.

📈 The UK’s optimal debt issuance strategy. I swear this wasn’t just an excuse to make a lame Wham!/WAM! joke.

📈 The US equity market is one of the least concentrated in the world. Really!

📈 Are lifers fueling the bond issuance boom? Financial regulations rule everything round me

The other public subsidy to borrowers is limited liability: encourages leveraging up to maximise the volatility and value of the put option that lenders have sold on the business